|

4.3

Depreciation Is Only

an Estimate

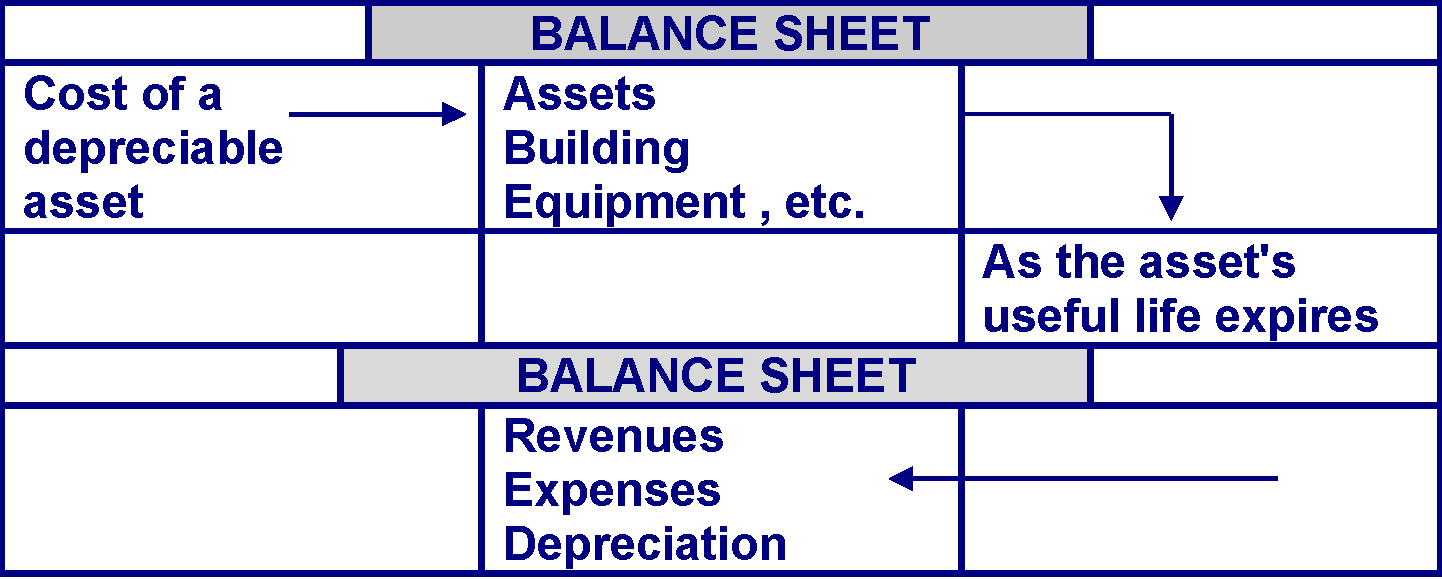

The appropriate

amount of depreciation expense is only an estimate. After all,

we cannot look at a building or a piece of equipment and

determine precisely how much of its economic usefulness has

expired during the current period.

The most widely used

means of estimating periodic depreciation expenses is the

straight – line method of depreciation. Under the straight –

line approach, an equal portion of the asset's cost is allocated

to depreciation expense in every period of the asset's estimated

useful life. The formula for computing depreciation expense

by the straight- line method is shown below.

Cost of the asset

Depreciation expense

(Per period) = --------------------------------

Estimated useful life

The use of an

estimated useful life is the major reason that depreciation

expense is only an estimate. In most cases, management does not

know in advance exactly how long the asset will remain in use.

How long does a

building last? For purposes

of computing depreciation expense, most companies estimate

about 30 or 40 years, but the empire state building was

built in 1931, and it's not likely to be torn down anytime soon.

And how about Windsor Castle? While these are not typical

examples, they illustrate the difficulty in estimating in

advance just how long depreciable assets may remain in use.

Example 4.1

Depreciation of

Summit's Building:

Summit purchased its

building for $36,000 on January 22. Because the building was

old, its estimated remaining useful life is only 20 years.

Therefore the building's monthly depreciation expense is $150

($36,000) cost ÷ 240

months). We will assume that summit did not record any

depreciation expense in January because it operated for only a

small part of the month. Thus the building's $1.500 depreciation

expense reported in summit's trail balance. An additional $150

of depreciation expense is still needed on the building for

December (bringing the total to be reported in the income

statement for the year to $1,650)

The

adjusting entry to record depreciation expense on summit

building for the month of December appears below:

Dec 31

Depreciation Expense: Building 150

Accumulated Depreciation: Building

150

Monthly depreciation on building

($36.000 ÷ 240 mo.).

The

depreciation expenses: Building account will appear in summit

income statement along with other expenses for the year ended

December 31, 2004. The balance in the Accumulated

Depreciation: Building account will be reported in the

December 31 balance sheet as a deduction from the Building

Account. As shown in the following:

Depreciation is not an attempt to record changes in the asset's

market value. In the short run, the market value of some

depreciable assets may even increase, but the process of

depreciation continues anyway. The rationale for depreciation

lies in the

|

Building

|

$ 36,000 |

|

Less : Accumulated

Depreciation Building |

(1,650) |

|

Book Value

|

$ 34,350 |

Accumulated Depreciation:

building is an example of a contra – asset account because (1)

it has a credit balance, and (2) it is offset against an asset.

Accountants often use the term book value (or carrying value) to

describe the net valuation of an asset in a company's accounting

records. For depreciable assets, such as building and

equipment, book value is equal to the cost of the asset, less

the related amount of accumulated depreciation. The end result

of crediting the Accumulated Depreciation: Building account is

much as if the credit had been made directly to the Building

account: so that the book value reported in the balance sheet

for the building is reduced from $36,000 to $34,350.

Book value is of significance primary for accounting purposes.

It represents costs that will be offset against the revenue of

the future periods. It also gives users of financial statements

an indication of the age of a company's depreciable assets

(older assets tend to have larger amounts of accumulated

depreciation associated with them than newer assets). It is

important to realize that the computation of book value is based

upon an asset's historical cost. Thus, Book value is not

intended to represent asset's current market value.

Example

4.2

Depreciation of Tools and Equipment

Summit depreciates

its tools and equipment over a period of five years (60 months)

using the straight – Line method. The December 31 trial balance

shows that the company owns tools and equipment that cost

$12,000 therefore, the adjusting entry to record December's

depreciation expense is:

Dec 31

Depreciation Expense: Tools and Equipment

Accumulated Depreciation: Tools and

Equipment

Monthly deprecation of tools and

equipment

($12.000 ÷ 60 months = $ 200

mo.)

Again, we assume that Summit did not record depreciation expense

for tools and equipment in January because it operated for only

a small part of the month. Thus, the

related $2,000 depreciation expense reported in. The tools and

equipment still require an additional $200 of depreciation for

December (Bringing the total to be reported in the income

statement for the year to $2,200).

What is the book value of Overnight's tools and equipment at

December 31, 2004? If you said $9,800, you're right.

|